Answering your top questions about Google’s advertising technology

We know there’s sometimes questions about Google’s advertising technology services (known as ‘Ad Tech’), and where they fit within the broader digital ads landscape.

What is ad tech?

Ad tech helps enable the buying and selling of advertising space on websites and apps, allowing content creators to increase ad revenues by connecting advertisers to their audiences. Google's investments in this space help publishers make money to fund their work, make it easy for businesses large and small to reach consumers, and support the creative and diverse content we all enjoy.

Where does Google fit in the ad tech industry?

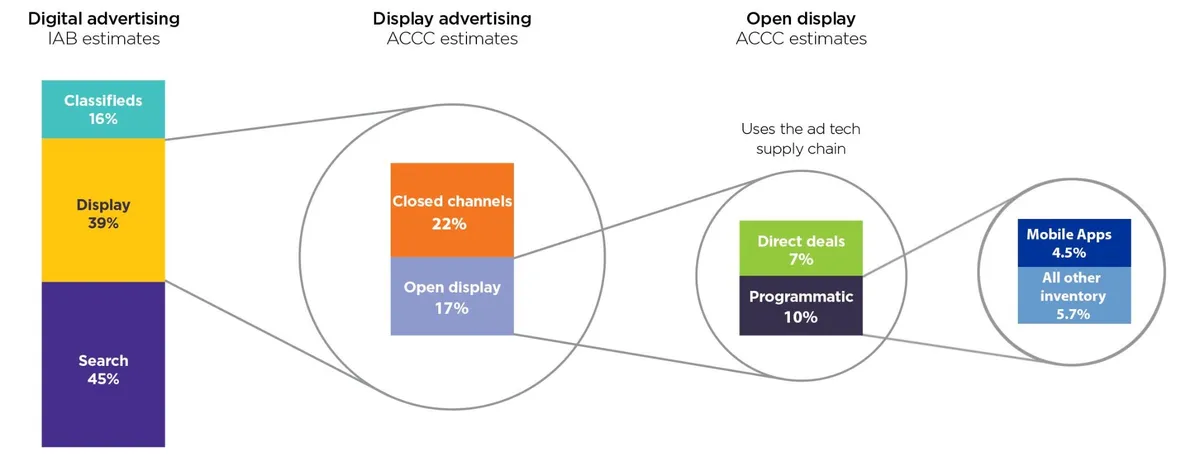

The digital advertising industry is dynamic and crowded, providing publishers and advertisers with enormous choice for displaying digital ads. Google’s ad tech products compete directly with what the ACCC in a recent report on digital advertising services refers to as ‘closed channels’ (for example, social media platforms like Facebook, Twitter, Instagram and TikTok), which are the most common way to buy display advertising. In fact, the ACCC found these represented 22 percent of total digital advertising (and 57 percent of total display advertising) spend in Australia in 2020.

Caption: This diagram above breaks down the different digital advertising channels in Australia by estimated size as a percentage of total digital advertising spend

(based on the ACCC Digital Advertising Services Inquiry Final Report).

What the ACCC refers to as ‘open display’ advertising, which has been the focus of the ongoing ACCC Digital Advertising Services Inquiry, was found to represent only about 17 percent of total digital advertising spend (and only 10 percent of total digital advertising spend depending on ‘programmatic’ channels provided by ad-tech vendors).

While ‘open display’ channels are only a small portion of the digital advertising ecosystem, globally there are many large and small, working together and in competition with each other to power digital advertising across the web. This includes household names such as Adobe, Amazon, AT&T and Facebook, as well as well-known industry players like Amobee, Criteo, Pubmatic, Magnite and The Trade Desk, among many others.

It also includes intense competition for open display ads within the fast growing areas of mobile apps and Connected TV (CTV), with apps making up 44 percent of what the ACCC has defined as the ‘programmatic open display channel’ (or 4.5% of total digital ad spend) based on the ACCC’s report.

Publishers and marketers have enormous choice when it comes to ad tech. A 2020 survey showed the average large publisher uses six different supply-side platforms (SSPs) to sell ads on its properties, and plan to use even more this year. The ACCC also found that there are nine demand-side platforms (DSPs) operating in Australia, together with closed channels like Facebook, all of which compete with Google for advertiser customers. A survey of marketers this year found that they intended to use on average six DSPs in the next 12 months.

How do Google's ad tech services help businesses?

Google’s ad tech helps websites and apps make money and fund high-quality content. It also helps our advertising partners reach customers and grow their businesses, achieving results in a cost-effective and efficient way. This is particularly true for small and medium-sized businesses (SMBs).

Analysis by PwC Australia found that three quarters of Google’s ad tech customers in Australia are SMBs. And almost three in four businesses surveyed saw important benefits from using Google’s services including cost savings, time savings and business growth, compared to other services—benefits that ultimately flow on to consumers. PwC also estimated that Google’s advertising technology directly supports more than 15,000 full-time equivalent jobs in Australia and contributes $2.45 billion to the Australian economy annually.

Are Google’s ad tech fees high?

The facts don’t support this. The UK Competition and Markets Authority (CMA) found that Google’s ad tech fees are consistent with industry averages. When marketers and publishers use the full range of our tools, most of the money goes from advertisers to publishers. For example, in 2019, when marketers used Google Ads or Display & Video 360 to buy display ads on Google Ad Manager, publishers kept over 69 percent of the revenue generated. And many publishers keep over 95 percent of the revenue generated when using our Ad Manager platform to sell ad space on their websites and apps.

The ACCC also found that average industry fees for DSP services had remained steady in Australia from 2017-20 and, in the case of SSP services, had actually dropped by 20 percent. That’s more money in publishers’ pockets to fund their creation of high-quality content.

It’s important to note that revenue shares include the costs of providing the services and enabling innovations that increase publisher revenue and maximize advertiser return on investment. They aren’t simply a profit margin for Google.

Does Google receive a data advantage in ad tech?

No - as we have explained to the ACCC, internet users are allocated into audience categories for the delivery of relevant ads on third-party websites and apps based primarily on their activity on third-party websites and apps. For example, if a user visits a third-party sports website, the user may be assigned into an audience of sports enthusiasts. Advertisers, like manufacturers of sporting goods, can then reach that audience on other third-party websites. This third-party data is not exclusive to any company, and a wide range of firms, including significant platforms such as Facebook, Apple, Amazon, and others, also collect such data for serving ads.

Google has always had policies and practices to safeguard the use of people’s data. And we have explicitly stated that once third-party cookies are phased out of Chrome, we will not build alternate identifiers to track individuals as they browse across the web, nor will we use such identifiers in our products.

Building on this principle, the commitments we’ve recently offered the CMA confirm that once third-party cookies are phased out, we will not use Google first-party personal data to track users for targeting and measurement of ads shown on non-Google websites. Our commitments would also restrict the use of Chrome browsing history and Analytics data to do this on Google or non-Google websites. If the CMA accepts these commitments, we will apply them globally.

What is the Privacy Sandbox and will it give Google an advantage in ad tech?

The Privacy Sandbox initiative aims to develop new technologies to protect user privacy and prevent covert tracking, while supporting a thriving ad-funded web. From the start of this project, Chrome has worked with the industry to develop these technologies in the open, and sought feedback at every step to ensure that they work for everyone, not just Google. All web community members and industry stakeholders, including other browsers, online publishers, ad tech companies, advertisers and developers are invited to participate in this collaborative process. This means these technologies can also be adopted by competing browsers and ad tech providers. They will not be exclusive to Google Chrome or Google’s advertising business. Our proposed commitments make clear that, as the Privacy Sandbox proposals are developed and implemented, that work will not give preferential treatment or advantage to Google’s advertising products. So far, Chrome and other stakeholders have submitted more than 30 proposals for privacy-preserving technologies, which can be found in the public resources of W3C groups.

Has Google’s vertical integration across the ad supply chain created a conflict of interest?

While we offer tools for both advertisers and publishers, that doesn't mean we are conflicted. Our sell and buy side products are designed to increase publisher revenue and maximize advertiser return on investment respectively. Offering tools for both advertisers and publishers is also commonplace in the ads industry. As the ACCC’s own report shows, many competing ad tech businesses offer ad platforms and tools like ours that cater to both advertisers and publishers, including AdForm, Amazon, Xandr, and Innovid, among others.

We don’t require either advertisers or publishers to use our whole ‘stack’, and many don’t. Ultimately, advertisers and publishers can choose what works best for their needs.

We pride ourselves on delivering great quality products to our customers - whether they’re advertisers or publishers. Our products must serve the interests of our partners to remain viable.

Has Google’s vertical integration across the ad tech supply chain resulted in self-preferencing behaviour?

Our products compete on their merits, and we strongly reject any suggestion we’ve engaged in harmful self-preferencing in our supply of ad tech services, or that our practices restrict competition.

We make product decisions and changes to better our services, including improving quality, reducing costs, preventing fraudulent ads, and strengthening data protection - often in response to requests from our customers. Vertical integration is a way of better coordinating different technology solutions to serve advertiser and publisher needs and facilitate ad campaigns.

In fact, many submissions to the ACCC acknowledged vertical integration can create efficiencies in the supply chain and provide benefits to advertisers and publishers - and that many industry participants agree. For example, the A&A have said businesses wanted ad tech to be more closely integrated to improve turnaround times, reduce costs and protect publisher inventory, and that Google “took this feedback seriously”. Omnicom Media Group shared that campaign implementation is easier for advertisers when using vertically integrated service providers, and that vertically integrated providers are able to provide superior inventory forecasting and delivery of programmatic guaranteed deals to publishers. SBS has said that vertical integration provides more ‘streamlined operations’ for users, and The Guardian observed that our integration of AdX into Google Ad Manager makes it easier for publishers to set up and run programmatic guaranteed campaigns, which can otherwise be a very manual and time consuming process.

How is Google supporting transparency in the ad tech ecosystem?

We welcome measures that increase transparency and trust in the digital ads ecosystem. Our products include a number of features that help publishers better understand how their inventory was sold and make informed decisions about the pricing of their inventory. This includes granular impression data in Google Ad Manager’s Data Transfer Files, as well as features like ‘Minimum Bid To Win’, which gives buyers insight into the minimum amount they would have needed to bid in order to win the auction. And in another recent development, Google Ad Manager reports can include “bid range” dimension (currently in beta), which shows the bid range for the publisher’s inventory. These reports can also show “bid rejection reason,” which is the reason why the bid for a publisher’s inventory lost.

We have also been actively participating in a number of industry initiatives to increase data available for advertisers, such as ads.txt / app-ads.txt, seller.json and SupplyChain Object specifications. These initiatives provide advertisers with a greater visibility into the overall supply chain, which can help them inform future buying decisions.

We look forward to continuing our work with other industry participants on data solutions, in a way that does not compromise user privacy or customer confidentiality.

How does Google think about regulation?

We support sensible regulation that tackles issues in a way that balances social needs, like free expression, diversity and innovation. We’ll continue our work to help publishers and advertisers grow with digital ads and collaboration with the broader industry and regulators on constructive solutions that support a healthy and sustainable ads ecosystem.